Have you heard talk recently about Tufts’ divestment plan? Are you left wondering what this all means? Discussions on divestment at Tufts have been occurring for years. From Tufts Climate Action’s first divestment campaign in 2012 and other campus groups showing support for divestment over the last decade, these efforts led to the Tufts Board of Trustees approving a sustainable investment plan for the university in February 2021.

The Office of Sustainability recently sat down with Craig Smith, Chief Investment Officer at Tufts, to learn more about this this plan, its effects on Tufts’ endowment, and get answers to common divestment questions.

Endowment? I think I heard about this on an episode of Succession….

First, let’s get some background on why Tufts invests in the first place. When donors give to Tufts, they can choose to have their money used today on immediate expenses for the university or they can donate to Tufts’ endowment.

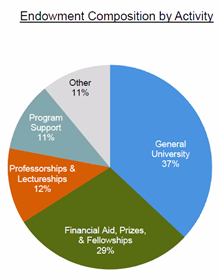

An endowment is a collection of charitable donations that provides long-term stability to support generations of students, faculty, and researchers equitably. This is done by investing Tufts’ endowment (roughly $2.7 billion as of June 2021) in the stock market and other securities, allowing it to grow, and withdrawing a small chunk of it each year (~5%) to help pay for university expenses (as shown in the pie chart).

Ultimately, a well funded and managed endowment supports student scholarships, innovative research, new areas of growth for the university, and more. Take three minutes to better understand the value of Tufts’ endowment with this video.

So, where’s the money going?

The Tufts Investment Office is tasked with managing the university’s endowment, with direction from the Board of Trustees and an Investment Committee, to make sure that it is invested in a way that provides long-term, equitable support for all generations of Jumbos.

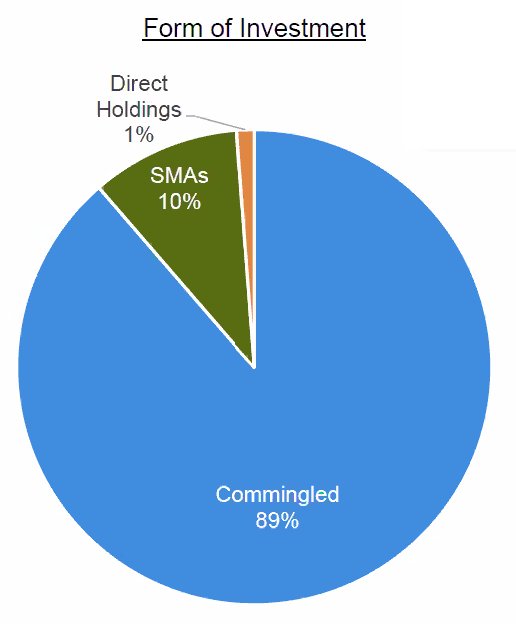

Right now, the endowment is invested in three categories. The smallest chunk (1%) is invested in direct holdings, which are individual stock investments that the university chooses directly.

Another 10% of is in separately managed accounts (SMAs). Tufts hires investment managers outside of the university, gives them investment goals and values, and those managers choose custom investments based on those criteria.

The largest portion of the endowment (89%) is in commingled funds. Investment managers outside of the university create funds to invest in many companies on behalf of many investors. This is, by far, the most common option available and typically the least expensive, although this is also the least customizable of the three options.

(Let’s pause to talk more about funds. Fund managers at investment firms – think Fidelity and Vanguard – gather stock in hundreds of companies to create a fund that is more stable than investing in an individual stock. Buying a fund is like buying a bag of M&M’s. You can’t walk up to the counter and ask that they remove all the brown M&M’s before you buy it…..Mars, Inc. just has too many customers to make you a special bag. Funds are similar. Many people buy into the fund so managers cannot accommodate every customer. Instead, they manage the fund independently and Tufts get a cheap and reliable investment.)

The scoop on divestment and other sustainable strategies at Tufts

In February 2021, Tufts announced the Responsible Investment Advisory Group’s (RIAG) guidelines to make the university’s investments more sustainable. They include:

- Divest from direct holdings and prohibit future direct investments in 120 coal and tar sands companies with the largest reserves. (Remember, direct holdings make up 1% of the money Tufts invests and is the easiest one to customize.)

- Invest $10 million to $25 million in positive impact funds related to climate change over the next five years. (More on this below)

- Proactively communicate with all current and future investment managers to encourage them to integrate climate values into their investment strategy

- Enhance transparency by creating a dashboard that would report on the university’s progress (The Investment Office just released the dashboard in November.)

- Evaluate progress on these guidelines.

The Investment Office is tasked with carrying out these actions and the university will revisit them in 2-5 years to analyze progress and make updates to the investment plan. The RIAG guidelines also call on the university to further integrate and advance their efforts on environmental sustainability across all disciplines.

Okay, here’s the TL;DR so far. Tufts has a $2.7 billion endowment that is held in investments and is a steady financial source to support Tufts forever. It’s invested in three ways: 89% in commingled funds (the least customizable), 10% in separately managed accounts, and 1% in direct holdings (the most customizable). Tufts released in Feb. 2021 guidelines for it’s investments including divestment from coal and tar sands in direct holdings and $10-25 million in positive impact investments.

Now that you’re an endowment expert, you might be left with other questions. How important are these investments for Tufts? Why are we only divesting our direct holdings? Why are we talking about M&M’s?

The Office of Sustainability hosted a webinar (viewable to the Tufts community) in December 2021 with Craig Smith, Chief Investment Officer at Tufts, to get into the nitty gritty of divestment, portfolio management, sustainable investing, and all those other financial buzzwords!

Q&A With Craig Smith

What impact does selling a company’s stock have on the company?

“Generally, not very much. When buying and selling stocks in the stock market the money from those transactions doesn’t go to the company. Most of the money a company raises from investors happens before being on the market and as it “goes public” (becomes listed on a stock exchange). Afterwards, when you sell a stock, you are selling it to somebody else, another investor, and so from the company’s perspective their balance sheet hasn’t changed a whole lot.

“When there is tremendous selling pressure that can push prices down temporarily, but you’re still selling the stock to someone who is buying it at that price, so it doesn’t really change things. As long as companies are making profit from what they’re doing, and certainly fossil fuel energy companies are making a profit from what they’re doing, that will allow the company to continue operating. Things that could change profit are regulations and alternative energy options. Having energy alternatives will impact how much revenue fossil fuel companies make.”

With sufficient time and a high level of commitment from Tufts, how would you achieve further divestment?

(Divestment is a pretty simple concept: selling existing investments in a particular area, in this case fossil fuel companies. In practice, it becomes more complicated.)

“It’s happening on three different levels at different paces. One is at the industry level. Companies are changing, so there will be less fossil fuel and greenhouse gas production as energy companies are making changes on their own front [to alternative energy].

“The second is around the managers that we invest in, as the [fossil fuel] decline happens in the energy space, managers will have less and less [fossil fuel investments] over time.

“And the third is managing the Tufts portfolio to reduce the exposure we have to certain investments where we have the most fossil fuel exposure. This is something we’re looking at today…in the commingled funds and looking at which of our managers make up the most of that exposure. The other thing that will bring this down over time is not making future private investments in the general fossil fuel energy space. We have not made a new private investment in this space for a few years and we will not make any moving forward.”

While Tufts has no direct holdings in the coal and tar sands companies identified in the RIAG guidelines, 0.7% of the money invested in commingled funds are still invested in these companies. You mentioned that to divest from this 0.7%, you’d have to liquidate ~20% of the holdings in the commingled funds, what is the implication of that?

(Remember the M&M analogy? With commingled funds, you can’t choose to exclude certain companies, you get whatever the fund manager decides to invest in. To exclude the 0.7% of the endowment invested in coal and tar sands companies held within some funds, Tufts would have to sell all their holdings in those funds, ~20% of the total endowment.)

“It’s hundreds of millions of dollars that we would sell from our portfolio and those are from managers that we view as best in class. So, we would expect to lose value in the portfolio.” (aka less money in the endowment for the expenses in the first pie chart above). “The bigger challenge is the secondary and tertiary effects. If we did that once and reinvested the money in other funds, there may be managers we use that may not be invested in these companies today, but may be tomorrow. It makes it really difficult to be long-term invested when you don’t know if you may have to liquidate a fund tomorrow.”

What about the fossil fuel companies that are not involved with tar sands and coal, how come we didn’t divest from them?

“That was an area of a lot of debate. There were many discussions on where to draw the line. It becomes complicated when you try to define what a fossil fuel company is – some companies do many things including fossil fuel, so you need a clear definition when making a plan. The driver around not including natural gas and oil [in the RIAG guidelines] had to do with the energy sector transition. Coal is actively coming down in usage because we have natural gas as an alternative for generating energy and heat. So that fossil fuel still has a place in the energy transition because it’s beneficial in how it’s replacing coal, which for the next few years is still a positive as there is not sufficient capacity yet in alternative energies. There was a lot of discussion around this and ultimately it was decided that natural gas was a necessary bridge to get to where we need to go.”

Does Tufts hope to increase positive impact investments over time beyond the $10-25 million in the RIAG guidelines?

(Positive impact investing is a strategy to invest in a way that furthers a social or environmental goal. The most impactful type of these are private investments – not traded publicly on the stock market – as the money goes directly to the company to help build their business. For example, Tufts could invest in a growing solar company. An investment like this helps build solar energy infrastructure, is a financial benefit, and can help lessen our dependence on fossil fuels, like natural gas.)

“I think that will definitely be what we talk about at the RIAG review in a few years. There is certainly a good case to be made for this type of investment over the long-term because it’s a growth area and as the alternative energy sector matures, there is less risk with investing in it. There are also more and more investment managers who are experienced in positive impact investing and the quality of these managers is increasing rapidly as well.”

Could money from commingled funds that contain the 0.7% of coal and tar sands companies be instead invested in positive impact investments?

“It’s not a 1 to 1 trade off. The timing of these two types of investing are different. A lot of what we’re doing in the positive impact investments are private investments because that’s where you have more impact as opposed to public investments. When you invest in the private space the money is actually going to the company and truly helps these companies develop.”

How does Tufts compare to other schools’ divestment plans? Are we running into the same problems?

“Yes, everyone is running into the same issue. The California school system has gone further, but they are also much larger with over $100 billion and so they do a lot more in that customizable SMA category, which gives them greater flexibility. But with endowments of comparable size to Tufts, everyone runs into the same issue with commingled funds. What you see in divestment announcements from other universities is around direct holdings, putting positive impact dollars to work, talking to managers they work with and trying to limit exposure that way – those are the vast majority of actions taken by universities of our size, including Tufts.”

How do we find the most up to date information about the components of Tufts’ investment portfolio?

“Our investment office dashboard is live as of November. There is additional information in an annual report (FY 2021 report coming soon!) that covers performance and allocation that is also posted on our website.”

Find Us On Social Media!