China leads in localized AI chip supply chain; US lags behind

Chris Miller, Professor of Tufts University, Author of ‘Chip War’

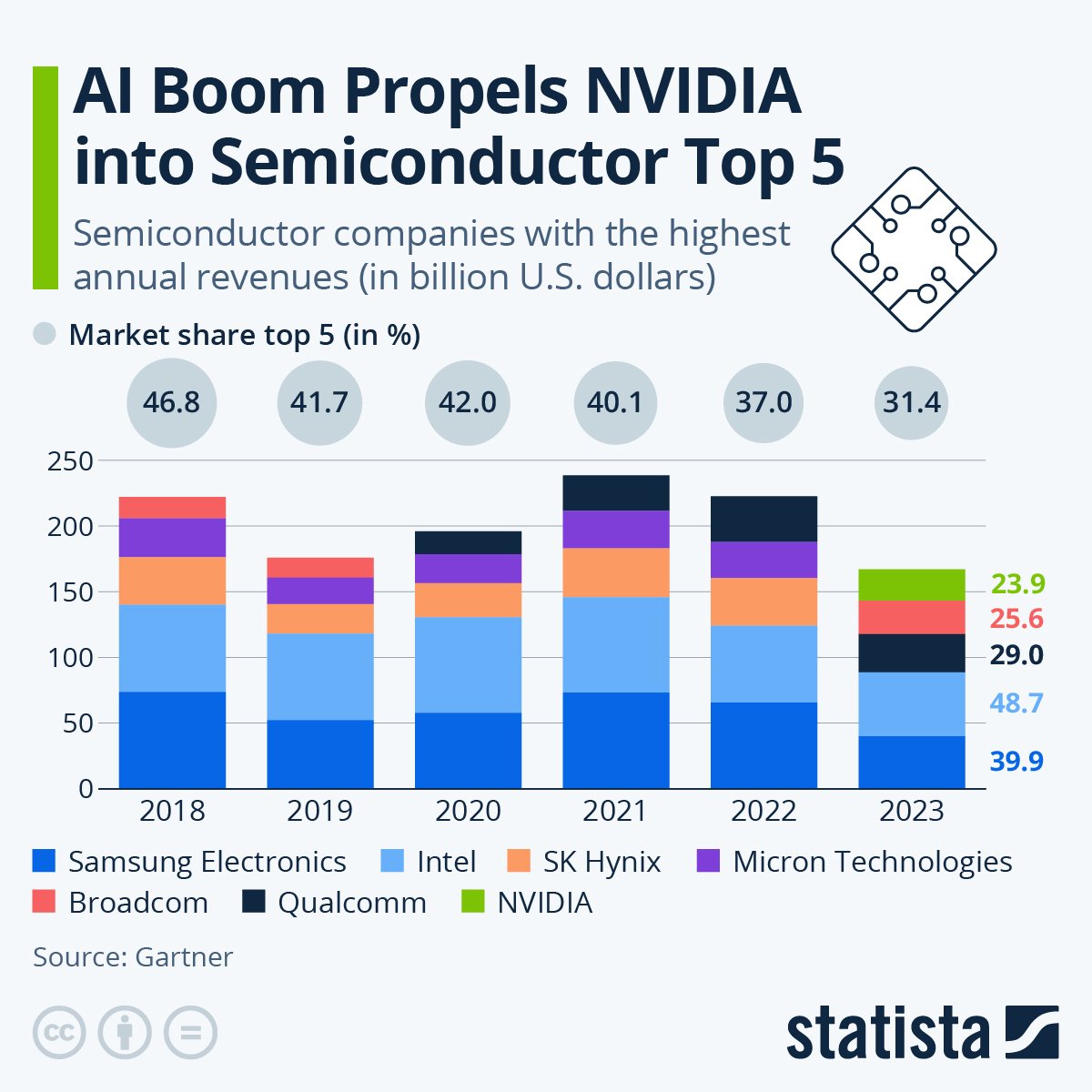

The third chip war: China vs. US for supply chain localization, Samsung and SK Hynix in DRAM, and US tech giants vs. Nvidia’s GPU.

By Sejin Kim, featuring Chris Miller, Associate Professor of International History at The Fletcher School, and author of Chip War: The Fight for the World’s Most Critical Technology

The global race for semiconductor supremacy has the potential to reshape the balance of power in the 21st century, with the United States and China locked in a high-stakes battle that could redefine the future of technology, innovation, and geopolitical influence.

The Third Semiconductor War is unfolding. Following 15-year cycles focused first on PCs and then smartphones, artificial intelligence has now taken the baton. In an exclusive video interview, Chris Miller, a professor at Tufts University, emphasized that true competitiveness lies in technological superiority, not just localized production.

Miller argues that while nations worldwide subsidize domestic semiconductor manufacturing, this approach has its limits. “The success or failure of any semiconductors, including South Korean chip companies, is primarily decided not by whatever subsidies they receive, but rather by clever technology,” Miller stated. He mentioned that in the memory chip space, Samsung has traditionally been the biggest player, but over the last year, SK Hynix has outperformed it by producing the most advanced type of DRAM, known as high-bandwidth memory (HBM) chips, crucial for AI processing. “Governments must realize that their role is at best as a helper. The success or failure of their efforts won’t be determined by the amount of spending but by the efficacy of the companies’ R&D efforts.”

A notable point is that China is one of the few countries that has successfully localized its supply chain. China has now localized much of its supply chain, posing a direct challenge as the world’s two superpowers jockey for semiconductor supremacy in the emerging AI era. At the same time, the traditional hierarchy is being disrupted, with South Korean upstart SK Hynix surpassing long-dominant Samsung in advanced high-bandwidth memory chips coveted for AI applications.

🌡️ [Preview] The Future of AI Semiconductors: The Mill asks, Chris Miller answers

- Has Samsung Semiconductor lost its competitive edge?

- Will Korea’s 26 trillion won investment be effective?

- Are US sanctions on China’s semiconductors effective?

- Will Nvidia’s dominance continue?

- Where is the battleground for the future semiconductor war?

(출처 : Statista)

Signs of Change in the Global Supply Chain

Since ChatGPT’s launch in November 2022 sparked an AI boom, global competition to develop AI models has intensified, explosively driving demand for the semiconductor chips essential for training.

The industry broadly splits into ‘processors’ or ‘logic chips’ for computations and ‘memory’ chips for storage. Companies designing processors like Nvidia, AMD, Micron, ASML, and Microsoft have soared in value.

In Asia, manufacturers have emerged to produce these designed chips, forming a global supply chain. Taiwan’s TSMC dominates chip fabrication, assembling and producing logic chips designed by firms like Nvidia. South Korea’s Samsung and SK Hynix monopolize the DRAM memory chip market, which along with NAND storage chips, stores the vast data processed by AI algorithms. Japan excels in semiconductor materials and equipment production. China leads in optoelectronics chips. Malaysia, the Philippines, Thailand, and Vietnam participate in assembly. India has broader ambitions, with “generous” incentives aiming to build fabrication facilities and a full supply chain beyond just assembly, according to Miller.

The UAE has poured investment into AI startups and developed its own model with a firm called G42. However, Miller says “there’s no semiconductor production nor any concrete plans yet reported in the UAE beyond just ideas floated publicly.”

This semiconductor supply chain now faces tectonic shifts.

Miller had a different assessment of China’s progress. “China has tried to localize its supply chain as much as possible and has seen genuine success,” he said, noting SMIC’s continuously improving capabilities and competitive memory chips from YMTC. (출처 : Sejin Kim)

The Global Trend to Localize, but Technology Leads

Governments in the US, China, Taiwan, South Korea, and others push to localize supply chains, viewing semiconductors as strategic national assets and security priorities—silicon as hard power. The US introduced its $52 billion CHIPS Act with subsidies and tax incentives, while South Korea recently unveiled a $19 billion support package.

However, Miller is skeptical of this policy approach. While some chips like automotive semiconductors tend to be produced regionally, he notes: “Each country is attempting to localize its supply chain, but it doesn’t seem likely to succeed. Despite substantial support from governments in the US, Japan, Europe, and other regions, memory chips are still mostly produced in South Korea. This is unlikely to change soon.”

More critical than subsidies is technological prowess. “The success or failure of any semiconductors, including South Korean chip companies, is primarily decided not by the subsidies they receive, but by their clever technology,” Miller stated. “For example, Samsung is the biggest player in the memory chip sector, but over the last year, SK Hynix has been the best performer because of its ability to produce the most advanced type of DRAM—their high-bandwidth memory (HBM) chips used in AI processing.”

He continued, “Government investment can help, but it does not guarantee technological leadership. Companies create innovations through R&D, and the government is just a supporter. Success or failure is determined not by the environment but by the outcomes of corporate R&D efforts.”

China’s Success in Localizing Its Supply Chain

However, Miller had a different assessment of China’s progress. “China has tried to localize its supply chain as much as possible and has seen genuine success,” he said, noting SMIC’s continuously improving capabilities and competitive memory chips from YMTC.

With China nearing full localization, can the US maintain its lead? Miller sees two major obstacles:

First are the sanctions from the US and its allies. “The US cannot control the outcomes, but it can create chaos. Due to US sanctions, SMIC, the most advanced chipmaker in China, is already experiencing substantial problems. YMTC would likely have grown larger without US restrictions, though there are practical limitations.” He added, “The US certainly has the power to disrupt the supply chain even if it can’t completely control it. All of China’s progress can cause real problems for Chinese firms. It can and it does.”

The second is the Chinese government’s own crackdown, with sanctions against the tech sector under pretexts like data protection. “Employees and investors have lost morale, and innovation capabilities are constrained. Compared to proactive big tech firms in the US, Chinese companies like Tencent and Alibaba are now far less dynamic.”

Microsoft CEO satya nadella and Nvidia CEO Jenson Huang (출처 : Microsoft)

The DRAM Story: Samsung and SK Hynix

The DRAM memory chip market illustrates the shifts. Long dominant, Samsung recently replaced the head of its semiconductor division after SK Hynix leapfrogged them by developing advanced high-bandwidth memory (HBM) critical for AI, securing major Nvidia supply deals.

Miller commented, “Samsung was not alone in failing to predict HBM would be so important right now. Even SK Hynix has been surprised by the demand for HBM, which is why they’ve been struggling to produce all the HBM that the industry has required.”

He added, “In HBM, SK Hynix has a significant edge currently. It would have been better if Samsung, Micron, and others accelerated HBM production to meet demand, but this situation doesn’t necessarily indicate a broader problem for Samsung.”

Samsung and Micron remain vital DRAM players, with Samsung likely the largest overall memory producer for some time given its scale advantage over SK Hynix and Micron.

Miller sees Samsung’s key challenge lying more in the fabrication or ‘foundry’ business, where TSMC dominates logic chip production. “Logic foundry is much more difficult. TSMC is the leading producer, and Samsung and Intel are fighting for a distant second place in the foundry market—a much less attractive position than memory.”

Stuart Pann (right), Intel’s Senior Vice President and General Manager of Foundry Services, greets Rene Haas, CEO of Arm, at the Intel Foundry Direct Connect event held in San Jose, California, on Wednesday, February 21, 2024. (출처 : Intel)

Nvidia’s Rise and Potential Competitors

Any discussion of AI semiconductors must include Nvidia, whose accelerator chips bundling specialized GPUs for AI training have unlocked large language models, reshaping the market.

“Currently, Nvidia holds a very strong position,” Miller noted. “Even if AMD makes chips with the same performance, Nvidia has a much more advanced ecosystem with CUDA cores acting like a lock-in, similar to Apple’s iOS—using other AI chips would require switching software stacks.”

Still, Nvidia’s $200+ billion valuation will inevitably attract competition from two groups, according to Miller:

The first: direct rivals like AMD and Intel.

The second: major customers like Google, Amazon, Microsoft, and Facebook designing their own accelerators already used internally. “Big tech companies receive less attention but might actually in the long run be more important to Nvidia because if companies use their own chips, they’ll buy fewer Nvidia GPUs.”

Nvidia exemplifies the emerging “law of Huang”—memory capacity doubling yearly—succeeding Moore’s law of transistor density doubling biennially. “Nvidia has benefited from traditional Moore’s law, but their unique processor functions designed for specific AI tasks far outperform traditionally designed CPUs,” Miller said. “The entire industry will enhance chip specialization and efficiency.”

Intel focuses on ARM-based CPUs, challenging x86’s laptop dominance, plus scalar accelerators for data centers. “It’s no coincidence Intel’s CEO stood alongside ARM’s at a recent event—Intel realizes the x86 ecosystem is going to become less important over time.”

The Next 15 Years: Post-GPU Future

While AI ushered in a new semiconductor phase after PCs and smartphones, Miller cautions “there will be ups and downs, not just an upward trend.” Today firms spend billions on cutting-edge Nvidia GPUs—the bottleneck for operating AI systems.

He identifies data centers, chip design, and software as areas for coming investments, predicting “massive” GPU data center buildouts. “In the short term, the most disruptive tech will likely be chip design and software with their shorter product cycles affecting various suppliers’ market share.”

Longer-term, he watches for new architectures improving performance and efficiency. “There’s no doubt GPUs won’t be the end—something else will come along in 5-10 years to create the ‘faster AI processing’ everyone wants by improving energy use.”

‘Chip War’ features narratives around seminal figures like Intel’s Andy Grove and TSMC’s Morris Chang. The current pivotal player, Miller says, is Nvidia CEO Jensen Huang. “Nvidia is at the center of new semiconductor investments for AI chips. How this unfolds will depend greatly on Jensen Huang and Nvidia.”

Note: This article is a slightly modified translation of the original Korean articleby reporter Sejin Kim using generative artificial intelligence (AI). The Miilk not only covers generative AI, but also experiments with using generative AI solutions to create actual content.

We look forward to hearing your thoughts on this emerging technology and its potential impact, please drop us a line at sejin@themiilk.com.

(This post is republished from The Milk.)