How Sanction-Proof is the Russian Economy?

By Chris Miller, Assistant Professor of International History at The Fletcher School of Law and Diplomacy at Tufts University

The Issue:

The United States and the European Union have reacted to Russia’s invasion of Ukraine by imposing a range of economic sanctions. Despite the Russian government’s claims to have “sanctions-proofed” its economy by accumulating a large stock of foreign currency reserves and developing alternative payments mechanisms, financial sanctions are already proving to be a powerful economic weapon. Russia’s currency has slumped, financial markets have faced distress, and factories have been shuttered. Whether the sanctions induce the Kremlin to change its foreign policy remains to be seen.

So long as Russia is willing to spend substantial sums on its foreign policy we should expect Russia to pursue broader foreign policy aims than the moderate size of its economy might suggest.

The Facts:

- Even before Russian troops entered Ukraine this year, Russia had pursued policies to protect its economy from the impact of sanctions. There was precedent: Sanctions were imposed on Russia after it annexed Crimea and invaded the Donbas region of Ukraine in 2014. These sanctions banned all foreign business in Crimea, prohibited the transfer of advanced oil drilling technology to Russia, and limited the access of major Russian firms to Western capital markets. These sanctions had a minor adverse impact on Russian oil production and a slight negative impact on investment in Russia and economic growth. The Russian government knew that the West might impose additional sanctions and therefore tried to insulate its economy from such measures. This has been called the “Fortress Russia” strategy. It includes efforts to limit foreign debt, amass central bank reserves of foreign assets to support the value of the ruble, and the creation of domestic payments systems in case Russia faced sanctions that severed its access to foreign bank transfer mechanisms like SWIFT (see here). The cost of these measures was substantial, because the government put funds into reserves, saving them rather than spending or investing them on immediate needs .

- The efforts to “sanction-proof” Russia’s economy from financial pressure prior to the invasion of Ukraine had limited success. Long-term investment from the West has not declined over the past decade. SWIFT and other non-Russian financial messaging systems, vital for international transactions by banks and even for the use of credit cards within Russia, conveyed about five times as many messages as MIR in 2020. The Russian central bank held about half of its foreign reserves outside the country at the time of the invasion of Ukraine. The Russian government also talked about reducing its reliance on foreign technology, but made little progress. “Import substitution” — the reduction of imports by boosting domestic production — has been a popular political slogan in Russia. However, it has had limited impact in reducing Russia’s integration with international supply chains or in reducing imports of capital equipment and machine tools.

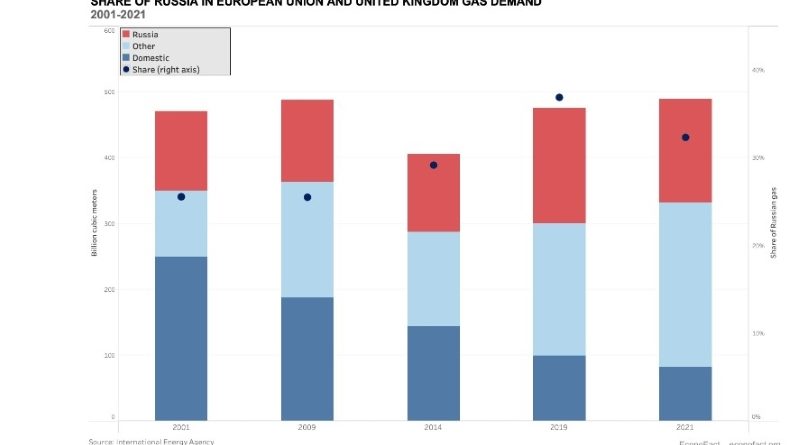

- The extent to which current sanctions are likely to impact Russian exports depends, in part, on the way in which they are traded. Oil is Russia’s most important export by far, accounting for nearly half of export earnings, depending on the oil price. Russia exports oil to many different countries and because oil is largely traded via ships — which can straightforwardly sail to any port — if one country stops buying Russian oil, Russia can usually sell to other buyers. As a result, the U.S. government’s recent decision to ban Russian oil imports to the U.S. will have a limited effect. The U.S. will increase oil purchases from other oil exporters; other oil importers will buy more Russian oil. Russia also exports a substantial amount of coal, which — like oil— is traded globally and so if one country stops buying Russian coal (the U.S. has banned imports) Russia can straightforwardly sell to other countries. It is a different story for natural gas, which is Russia’s second largest export. Most of Russia’s natural gas is exported to Europe, via pipelines that transit Ukraine, Belarus, and the Baltic Sea (Nord Stream I). Russia also has a gas pipeline that goes to China as well as some facilities to liquify natural gas, which allows it to be shipped worldwide. The existing pipeline and liquification infrastructure is limited, so the gas fields that currently supply piped gas to Europe have no other outlet if Europe stops buying Russian gas. This is a major vulnerability for Russia’s gas industry. However, it is also a weakness for Europe, which is reliant on Russia for natural gas imports: the share of Russian gas in European Union and United Kingdom supplies increased from 25% of the region’s total gas demand in 2009 to 32% in 2021, according to the International Energy Agency (see chart). Countries like Germany and Italy have long bought gas from Russia and lack the liquification infrastructure to acquire sufficient quantities of liquified natural gas from other sources. If they were to stop buying Russian gas — or if Russia were to stop selling — energy prices would spike and certain energy intensive industries might have to shut down.

- Russia’s dependence on imports also makes it vulnerable to sanctions. Russia imports many consumer goods and industrial products, including technology and machine tools. Russia has a manufacturing base that it inherited from the Soviet Union, but most of the manufacturing sector that remains is now deeply integrated with international supply chains. Because of this, Russia is heavily dependent on access to components and tools from the U.S., Europe, Japan, South Korea, and Taiwan. The auto industry, aviation industry, and other manufacturing sectors will struggle to function in the absence of components from Western countries and their allies in Asia. Many Russian car factories across the country have already been shuttered due to component shortages. All types of complex manufacturing will face wrenching delays. Sectors like aviation manufacturing, which are subject to harsh restrictions, may struggle to produce any goods at all.

- Western companies have withdrawn from the Russian market, further harming Russian consumers. The closing of McDonalds across Russia is a high profile example of Western firms leaving Russian markets. The reduced availability of consumer goods — and the reduced diversity of products on offer — will leave Russian consumers less well off. No less important is the perception this will create among wealthier parts of the urban population in big cities like Moscow and Saint Petersburg, where the upper middle classes have become used to consumerist lifestyles. Now they will have a substantially more limited selection of goods available.

- The removal of business services from the Russian market will be even more disruptive. Russia is deeply integrated with Western markets for business services, from insurance, to finance, to logistics. One example is in aviation, where many planes in Russian airlines’ fleets were leased from aircraft leasing firms based in Europe. Sanctions prohibited such transactions and now a substantial share of the planes that used to fly in Russia are grounded or have been removed from the country. Spare parts will soon be a difficult issue as well.

- Sanctions on high-wealth and powerful individuals (“oligarchs”) are likely to have less of an effect on the economy. The Russian economy is marked by substantial inequality. Some U.S. and European sanctions target rich individuals, often called oligarchs, who own large businesses in Russia. Most such individuals in Russia often have substantial assets abroad too, including real estate in London or New York. The effect of seizing these assets, while damaging to these individuals, is not likely to have a major impact on the Russian economy as a whole.

What this Means:

It is already clear that western sanctions on Russia will have a major economic impact. Will they achieve their political goals? It seems unlikely that sanctions will reverse Russia’s invasion though by raising the cost they may make Russia slightly more amenable to compromise. Sanctions do seem likely to complicate the Kremlin’s domestic calculus, though typical Russians have few channels through which to express discontent. Sanctions will certainly make it more difficult for Russia to fund its foreign policy as well as to supply its military, given its reliance on Western technology for components, especially microelectronics and computing equipment. If the West intensifies sanctions by trying to sever Russian oil exports, this would cut off Russia from its primary source of export earnings. However, so long as Russia is willing to spend substantial sums on its foreign policy — far higher as a share of GDP than Western countries — we should expect Russia to pursue broader foreign policy aims than the moderate size of its economy might suggest. This may work in achieving Russia’s foreign policy aims, though the cost will be intensifying economic difficulties at home.

Editor’s note: Christopher Miller is author of “We Shall Be Masters: Russian Pivots to East Asia from Peter the Great to Putin“, Harvard University Press, 2021 and of “Putinomics: Power and Money in Resurgent Russia“, The University of North Carolina Press, 2018.

This piece is republished from ECONOFACT.